Testing times are ahead but there is hope for aggregates producers says Julian Clapp.

Hardly a day goes by without mention in the national news about the financial crisis facing Europe and the rest of the world.

Opinion seems to vary on a daily basis from some optimism to total pessimism. Investors hoping that markets will settle down soon are likely to be disappointed. Many of the financial arrangements currently being put into place involve the medium term repayment of loans. Unless the countries concerned are able to sort out their finances, further market turmoil can be expected for a number of years.

It is now generally accepted that countries such as Italy, Spain, Portugal, Greece and Ireland have to reduce their budget deficits. At the same time, analysts argue that countries should try to expand their economies so that Europe does not move into recession. Yet a reduction in government spending is likely to lead to recession, not growth. The only way this will not happen is if there is a major shift in public expenditure from current to capital expenditure.

Forecasts of economic growth in the current climate appear optimistic in the author’s view. These forecasts are issued to show how governments can escape large budget deficits without the need for further cutbacks in public expenditure which maybe politically unacceptable. An objective assessment of economic prospects is likely to show that economies will continue to stagnate for some time.

There is a strong preference amongst governments at the time of writing to maintain the Eurozone. However, capital markets may dictate that this becomes impossible: some countries leaving the Eurozone cannot be discounted.

Although the headline financial news will cause concern for some time to come, the effect on aggregates markets is likely to be more subdued. The European aggregates industry has already endured its fair share of recession. In 20 European countries, from Portugal to Poland, and including the major economies of Germany, France, Italy and the UK, volumes are down by an average of 25% since 2007. However, this masks significant differences between countries. In 2007, the size of the aggregates market in Poland was similar to that of Ireland. Yet by 2010, the Polish market was three times that of its Irish counterpart.

These market declines are much worse than the fall in GDP in any of these countries. This confirms that there is no longer a close correlation between economic output or even, construction output, and aggregates demand. Therefore, in future, a change in GDP or construction output may not necessarily result in aggregates demand changing in a similar way. The influence of individual end use markets, competing construction materials, recycled and secondary aggregates and taxes/levies all impact on demand, irrespective of the wider economy.

HOPEFUL VIEW

This de-linking between the economy and aggregates demand is one reason why

A number of major road schemes are planned in Poland and these will help push aggregates demand up by 20% in this country over the next few years. Volumes in the major countries appear to have bottomed out. A review of the financial performance of the top aggregates companies shows that turnover has increased by up to 10% in the first half of 2011. This tends to confirm that the worst of the recession is behind us, although some markets have drifted lower in the second half of 2011.

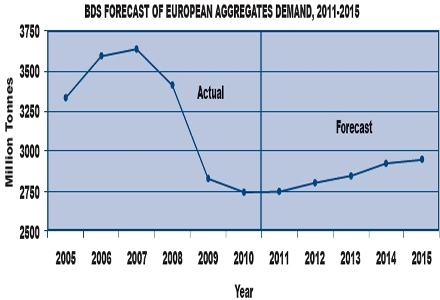

While there may be some further short term weakness in some countries, further falls in demand at the levels witnessed in recent years are not expected.

Projections are now based on levels of demand that are at historically low levels. By 2013, we are forecasting that aggregates demand in Europe will be nearly 5% higher than 2010 levels. The countries expected to perform best are Belgium, Poland, Sweden, the Slovak and Czech Republics and Denmark. However, the total market will still be below typical levels experienced in the last decade.

All major international aggregates companies have made structural changes to their businesses to cope with the new market situation. However, there are further actions which the sector needs to be taking.

It is the major international aggregates businesses that have the spread of operations and flexibility to cope in the current market. It is unlikely that acceptable offers for assets would be received currently in those countries deemed surplus to requirements. However, operations can be prepared for disposal once markets improve. Elsewhere, investment can be made in new reserves and smaller companies acquired in those countries considered having a long term future.

These larger companies need to assess strategy at both the international but also local level. Head office staff will assess the wider options. Local management needs to ensure that future reserves are guaranteed, quarries have the right capacity to meet local demand, and prices improve to recover higher energy and environmental costs.

Timing is key. Events in recent years prove this, if proof was needed. Some of the worst performing countries in recent years are possibly the ones that will recover the best. Although such recovery will be from very low levels, any improvement in markets will benefit the bottom line straightaway. Now may not be the time to exit the worst performing areas. It needs an objective analysis of current markets and future prospects to drive investment strategy.

It may be correct for one company to exit a poorly performing country but a competitor to maintain or even grow its operations in the same area. This will depend on an analysis of the relative value of downstream outlets, market share, cost base, reserves, acquisition possibilities and other factors.

MARKET SHARE

We estimate that the top 10 European aggregates companies now have a 23% share of the market. The top 10 ready mixed concrete companies (often the same businesses) have a 37% share of their market. Further development of aggregates’ operations can be expected to increase in-house purchasing of materials.

The influence of major aggregates companies varies considerably in Europe. In some countries, the top 10 companies represent around 80% of the market. Typically, the leading companies in Europe have around a half of the market, but in some countries, their share is as low as 20%.

By definition, countries where the majors already have a high market share offer fewer opportunities for growth through acquisition. Although countries with a low share offer the highest number of acquisition possibilities, it is likely that margins are low (with such a large number of competitors) and it would take many acquisitions to create a major player. The best option would appear to concentrate resources in a country where some companies are already established but a number of independent businesses still remain.

The table below shows, in order, our estimate of the market shares of the top 10 companies, from the highest to the lowest. The top 10 aggregates companies in some countries, for example Germany, have a relatively low share but their influence is higher, due to the number of joint ventures and minority shareholdings that some companies have.

Smaller, independent aggregates companies do not have the economies of scale but possibly know their local markets better and can respond flexibly to changes in market conditions.

The companies perhaps most in danger are those medium sized businesses, particularly those in countries which have performed poorly in recent years. Here, the formation of joint ventures with other companies, involving all or part of the business is one possible step forward. Historically, it is this sector which has seen a number of well-known businesses sold.

Both aggregates companies and industry associations need to stress to their governments about the benefits of investing in infrastructure during the recession. This is one of the most cost effective ways of boosting the economy. There is also a creeping trend of increased taxes, levies and environmental requirements in many countries, which the industry will do well to counteract.

In the past, markets in individual European countries have tended to move in tandem with each other. One result of the current financial crisis is that whist some countries are seeing aggregates markets decimated, others are escaping with little impact. The most successful aggregates companies will be those which can read the signals and plan accordingly.

Julian Clapp is founder and director of BDS Marketing Research, which regularly publishes reports on aggregates, ready mixed concrete, asphalt, concrete products, cement, waste and related sectors in the UK and Europe.

| Highest |

Netherlands | UK | Belgium | |||

| Above Average | Czech Republic | Sweden | Switzerland | Norway | ||

| Average |

Finland | Denmark | France | Austria | Ireland | Slovak Republic |

| Below Average | Portugal | Germany | Poland | |||

| Lowest | Greece | Italy | Spain | Turkey |

•Source: Report entitled: ‘An analysis of the markets for aggregates, ready mixed concrete and asphalt in 20 European countries’ published by BDS Marketing Research Ltd